Revenues Working Against WORK Medical Technology Group LTD’s (NASDAQ:WOK) Share Price Following 100% Dive

Share Price Following 100% Dive")

WORK Medical Technology Group LTD (NASDAQ:WOK) shareholders that were waiting for something to happen have been dealt a blow with a 100% share price drop in the last month. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 100% loss during that time.

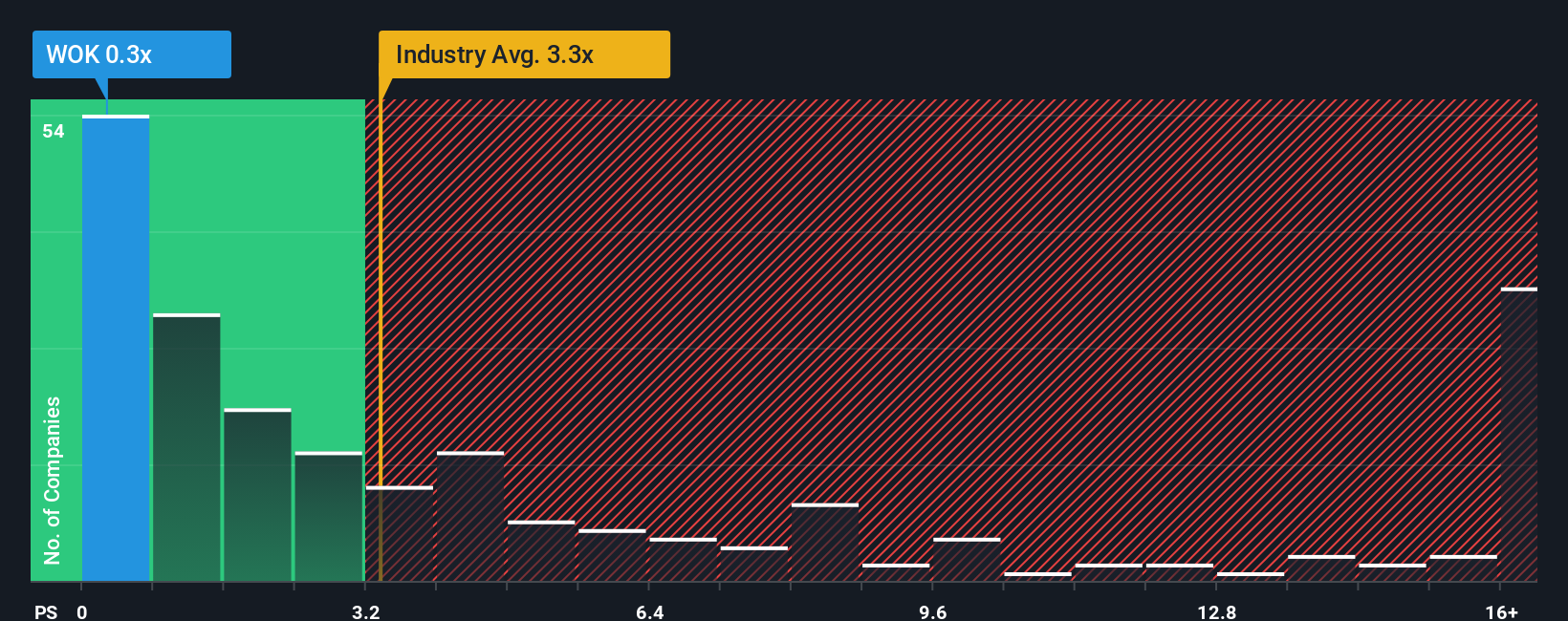

Since its price has dipped substantially, WORK Medical Technology Group may be sending very bullish signals at the moment with its price-to-sales (or “P/S”) ratio of 0.3x, since almost half of all companies in the Medical Equipment industry in the United States have P/S ratios greater than 3.3x and even P/S higher than 9x are not unusual. Nonetheless, we’d need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

View our latest analysis for WORK Medical Technology Group

What Does WORK Medical Technology Group’s P/S Mean For Shareholders?

Revenue has risen firmly for WORK Medical Technology Group recently, which is pleasing to see. Perhaps the market is expecting this acceptable revenue performance to take a dive, which has kept the P/S suppressed. Those who are bullish on WORK Medical Technology Group will be hoping that this isn’t the case, so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on WORK Medical Technology Group will help you shine a light on its historical performance.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

There’s an inherent assumption that a company should far underperform the industry for P/S ratios like WORK Medical Technology Group’s to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 8.9% last year. However, this wasn’t enough as the latest three year period has seen an unpleasant 44% overall drop in revenue. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Weighing that medium-term revenue trajectory against the broader industry’s one-year forecast for expansion of 50% shows it’s an unpleasant look.

With this information, we are not surprised that WORK Medical Technology Group is trading at a P/S lower than the industry. Nonetheless, there’s no guarantee the P/S has reached a floor yet with revenue going in reverse. There’s potential for the P/S to fall to even lower levels if the company doesn’t improve its top-line growth.

The Key Takeaway

Shares in WORK Medical Technology Group have plummeted and its P/S has followed suit. We’d say the price-to-sales ratio’s power isn’t primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of WORK Medical Technology Group confirms that the company’s shrinking revenue over the past medium-term is a key factor in its low price-to-sales ratio, given the industry is projected to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won’t provide any pleasant surprises either. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

It’s always necessary to consider the ever-present spectre of investment risk. We’ve identified 5 warning signs with WORK Medical Technology Group, and understanding them should be part of your investment process.

If you’re unsure about the strength of WORK Medical Technology Group’s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we’re here to simplify it.

Discover if WORK Medical Technology Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

link